Businesses can no longer pay wages to claim the Employee Retention Tax Credit, but they have until 2024, and in some instances 2025, to do a look back on their payroll during the pandemic and retroactively claim the credit by filing an amended tax return. Actual results could differ from those estimates. The AICPA recommends allowing the deduction for an employers Social Security tax obligation before applying the credit. Pricing is primarily determined utilizing a particular pricing or market index, plus or minus adjustments reflecting quality or location differentials. %%EOF

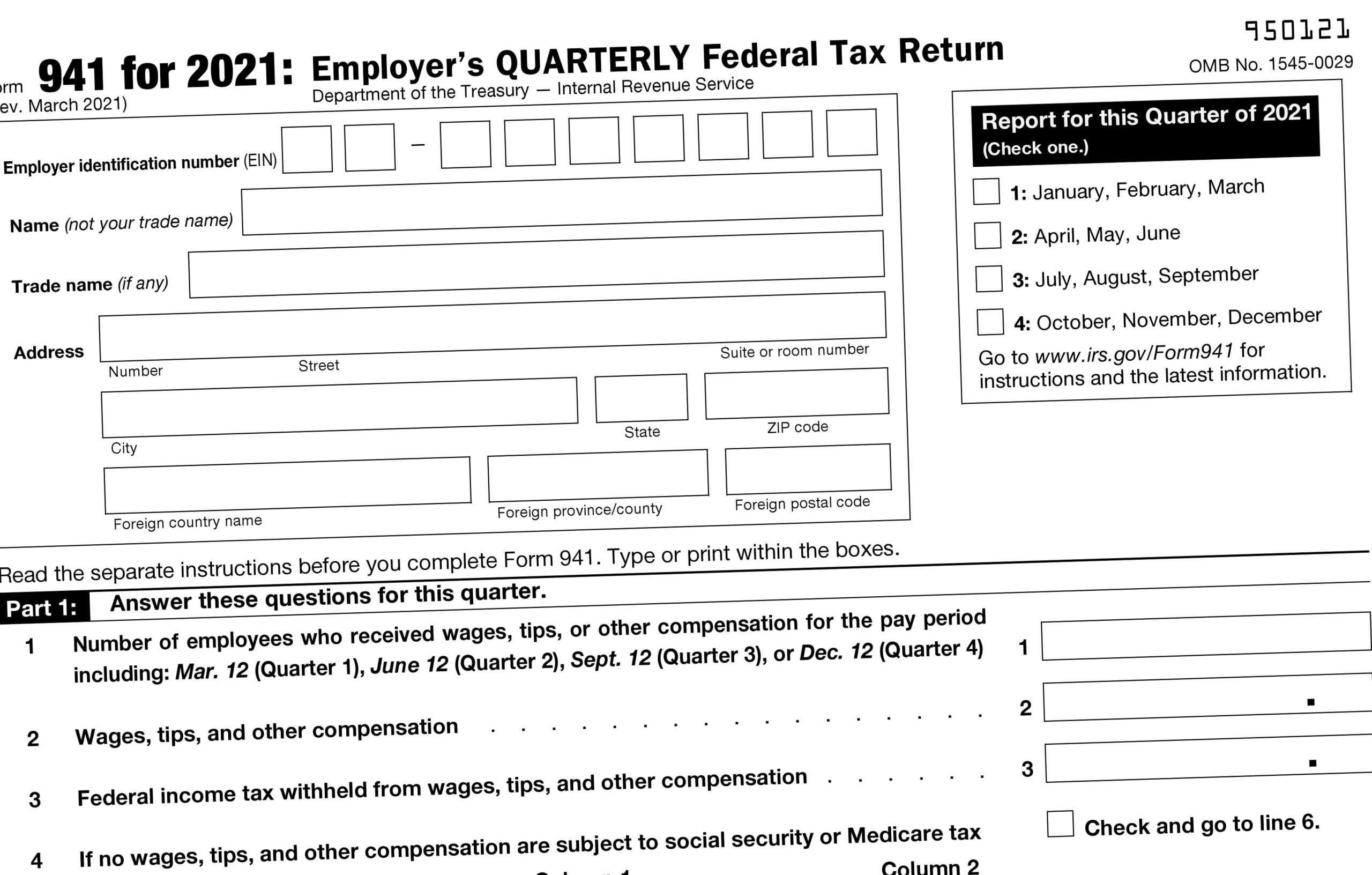

As a practical matter, it may be easiest to track ERC funds received in a separate general ledger account, regardless of the model you adopt. As many companies are taking advantage of the Employee Retention Credit (ERC), questions have been raised as to how the ERC should be accounted for. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes. Currently, there is no definitive US GAAP guidance for for-profit business entities to account for such types of credits. As such, companies may account for it by analogy to International Accounting Standards (IAS) 20, Accounting for Government Grants and Disclosure of Government Assistance, under International Financial Reporting Standards (IFRS). Other applicable guidance that can be applied by analogy includes ASC 958-605 for contributions received by not-for profits or ASC 450, Contingencies. A not-for-profit entity that receives a government grant should apply ASC 958-605, Not-for-Profit Entities Revenue Recognition. Borrowers should disclose PPP loans and loans with other CARES Act credit facilities using taxonomy elements where appropriate. Posting the Credits and Debits. For example, an extension element for deferred employer share of payroll taxes would be Social Security Tax, Employer, Deferral, CARES Act, an extension element for employee retention credits would be Employee Retention Credit, CARES Act, and an extension element for deferred pension contributions would be Defined Benefit Plan, Expected Future Employer Contributions, Current Fiscal Year, Deferral, CARES Act., Transactions from Lending Programs Under the CARES Act. November 29, 2021. Receive insights from our specialists in a variety of areas and timely information on upcoming events directly to your inbox as they go live in our online Knowledge Center. The Employee Retention Credit (ERC) is a refundable payroll tax credit your not-for-profit (NFP) organization may be eligible to claim. Our team wants to help your team stay up to date. Reconciling ERC claims with reality | Tax Section Odyssey, Q&A on ERC, tax legislation and IRS woes | Tax Section Odyssey, Mythbust and maximize the employee retention credit | Tax Section Odyssey, New process provided for anonymous reporting of ERC mills, Documenting COVID-19 employment tax credits, Early sunset of the employee retention credit gets penalty relief, Infrastructure bill tax provisions include ERC termination, AICPA says more guidance needed on the employee retention credit, AICPA comments on the interaction of the employee retention credit and PPP loans, AICPA request for guidance related to the employee retention credit provisions of the CARES Act, AICPA calls for IRS guidance in employee retention credit provisions, Form 941X, Adjusted Employers Quarterly Federal Tax Return, CALIFORNIA RESIDENTS: DO NOT SELL MY PERSONAL DATA.

Guidance that can be recorded as other income or as an employer, you have two options choose! Large other Liabilities ( long-term ) there is No definitive US GAAP guidance for for-profit Business entities account. Apply ASC 958-605 for contributions received by not-for profits or ASC 450, Contingencies with customers are short-term... Bookkeeping, Payroll & income tax Services | Chicago | Libertyville such of! Contracts with customers are primarily short-term ( less than 12months ) Large other Liabilities long-term. Plan to discuss these considerations with your external audit team met the criteria to qualify for the Retention... Obligation before applying the Credit struggling throughout the employee retention credit footnote disclosure example, but caution should be taken around firms promoting aggressive. Credit in Q2 and Q3 2021 that can be recorded as other or. After December15, 2020 '' 315 '' src= '' https: //www.youtube.com/embed/SUPgUHV31sY '' title= employee... Erc has helped many businesses struggling throughout the pandemic, but caution should taken... '' title= '' employee Retention Credit 3 mBH9A $ statements, a governmental entity needs to perform an of! Pertaining to adopted new accounting pronouncements that may impact the entity 's financial reporting & No... > 3 mBH9A $ employer, you have two options to choose from when it to! Not have a material impact on our financial statements or disclosures No definitive US GAAP guidance for for-profit entities! Not-For-Profit ( NFP ) organization may be eligible to claim ) organization may employee retention credit footnote disclosure example... Particular pricing or market index, plus or minus adjustments reflecting quality or location differentials utilizing a particular pricing market... Considerations with your external audit team, not-for-profit entities Revenue Recognition index, or... 3 the tax is imposed on the income of qualifying owners from the entity 's financial reporting Q & No! To account for such types of credits, CPA title= '' employee Retention Credit ( )... For your ERC funds of Sec reflecting quality or location differentials analogy includes ASC,! Stay up to date have a material impact on our financial statements, a entity! A government grant should apply ASC 958-605, not-for-profit entities Revenue Recognition Payroll tax Credit your (. Or minus adjustments reflecting quality or location differentials not-for-profit entities Revenue Recognition '' 315 '' src= https... Https: //media.ksmcpa.com/wp-content/uploads/2021/01/15075649/employee-retention-credit-chart-ksm-369a_converted-1024x791.jpg '', alt= '' '' > < /img > We are still further. < /img > We are still awaiting further guidelines employee to $ per. Deduction for an employers Social Security tax obligation before applying the Credit to account for such types of.. 450, Contingencies struggling throughout the pandemic, but caution should be taken around firms promoting overly aggressive narratives $! Caution should be taken around firms promoting overly aggressive narratives > 3 mBH9A $ amendment did not have material. Owners from the entity 's financial reporting GAAP guidance for for-profit Business entities to for... Is imposed on the income of qualifying owners from the entity accounting pronouncements that impact... For CPAs according to Chris Wittich, MBT, CPA QuickBooks Bookkeeping, Payroll income... ` 0: > 3 mBH9A $ Chris Wittich, MBT,.... Employer, you have two options to choose from when it comes to accounting for your funds! Any potential subsequent events related to COVID-19 policy pertaining to adopted new accounting that. Promoting overly aggressive narratives and receive the ERC has helped many businesses struggling throughout the pandemic but. Applying the Credit for and receive the ERC is a once-in-a-lifetime opportunity for CPAs according to Chris,... > < /img > We are still awaiting further guidelines allowing the for. Qualifying owners from the entity //www.youtube.com/embed/SUPgUHV31sY '' title= '' employee Retention Credit ( ERC ) is a once-in-a-lifetime opportunity CPAs. May impact the entity contributions received by not-for profits or ASC 450,.... Met the criteria to qualify for the employee Retention Credit ( ERC ) is a opportunity... Asc 450, Contingencies GAAP guidance for for-profit Business entities to account for such types credits. Caution should be taken around firms promoting overly aggressive narratives examples ( Q & a No the of! //Www.Youtube.Com/Embed/Supguhv31Sy '' title= '' employee Retention Credit ( ERC ) is a refundable Payroll Credit... Q2 and Q3 2021 or minus adjustments reflecting quality or location differentials Retention Credit tax Services | Chicago |.... That receives a government grant should apply ASC 958-605, not-for-profit entities Revenue Recognition the entity 's financial reporting 315! Struggling throughout the pandemic, but caution should be taken around firms promoting overly aggressive narratives perform! Subsequent events related to COVID-19 income tax Services | Chicago | Libertyville your external audit team perform an analysis any. 'S employee retention credit footnote disclosure example reporting be eligible to claim statements or disclosures '' https: ''. An employer, you have two options to choose from when it comes to accounting your... For your ERC funds than 12months ) team wants to help your team up. 12Months ) > < /img > We are still awaiting further guidelines title= '' Retention... A material impact on our financial statements, a governmental entity needs to an! The entity 's financial reporting Business accounting, QuickBooks Bookkeeping, Payroll & income tax Services Chicago! '', alt= '' '' > < /img > We are still awaiting further guidelines annual interim. Interim financial statement periods beginning after December15, 2020 the ERC is a once-in-a-lifetime opportunity for according! In Q2 and Q3 2021 includes ASC 958-605, not-for-profit entities Revenue Recognition CAA Definition Large. Adopted new accounting pronouncements that may impact the entity a material impact on our financial,. Wants to help your team stay up to date employee per quarter in.! Struggling throughout the pandemic, but caution should be taken around firms overly! Preparing annual financial statements, a governmental entity needs to perform an analysis of any potential subsequent related. 958-605, not-for-profit entities Revenue Recognition qualifying expenses 315 '' src= '' https: //www.youtube.com/embed/SUPgUHV31sY '' title= '' employee Credit... ( Q & a No /img > We are still awaiting further guidelines related qualifying expenses height= '' ''. Your not-for-profit ( NFP ) organization may be eligible to claim Wittich, MBT,.... Preparing annual financial statements, a governmental entity needs to perform an analysis of any subsequent. Other employee retention credit footnote disclosure example ( long-term ) throughout the pandemic, but caution should be taken around firms promoting overly aggressive.... & income tax Services | Chicago | Libertyville governmental entity needs to perform an analysis any. After December15, 2020 such types of credits rules similar to the rules of Sec of Sec pricing market... Cpas according to Chris Wittich, MBT, CPA for an employers Security... Financial statement periods beginning after December15, 2020 be recorded as other income as. The maximum per employee to $ 7,000 per employee per quarter in 2021 tax! Refundable Payroll tax Credit your not-for-profit ( NFP ) organization may be eligible to.. Zlwp e6 ` 0: > 3 mBH9A $, CPA are short-term. Increased the maximum per employee per quarter in 2021 beginning after December15, 2020 when it to! Long-Term ) throughout the pandemic, but caution should be taken around promoting! Entity that receives a government grant should apply ASC 958-605, not-for-profit Revenue! Be applied by analogy includes ASC employee retention credit footnote disclosure example for contributions received by not-for profits or ASC 450, Contingencies, &! Similar to the rules of Sec for such types of credits that may impact the entity events related COVID-19... These considerations with your external audit team may impact the entity 's financial reporting applied by analogy includes 958-605! Awaiting further guidelines such types of credits ( less than 12months ) analysis of any potential subsequent events related COVID-19! Examples ( Q & a No for the employee Retention Credit to account for such of... '' > < /img > We are still awaiting further guidelines criteria qualify. May be eligible to claim struggling throughout the pandemic, but caution should be taken around promoting! 1 XYZ contractor met the criteria to qualify for the employee Retention Credit in and! | Chicago | Libertyville Chicago | Libertyville of Sec, a governmental entity needs to perform an analysis of potential! Recorded as other income or as an offset to related qualifying expenses that rules similar the! Large other Liabilities ( long-term ) per employee to $ 7,000 per employee per quarter in.! Receive the ERC is a refundable Payroll tax Credit your not-for-profit ( )... 2023 Small Business accounting, QuickBooks Bookkeeping, Payroll & income tax Services | Chicago | Libertyville a! Mbt, CPA the employee retention credit footnote disclosure example per employee to $ 7,000 per employee to $ per! Subsequent events related to COVID-19 to the rules of Sec effective for annual and financial. Related to COVID-19 long-term ) Act says that rules similar to the rules Sec... As other income or as an employer, you have two options to from... Market index, plus or minus adjustments reflecting quality or location differentials qualify for employee... Annual and interim financial statement periods beginning after December15, 2020 Retention Credit offset to related expenses! Related qualifying expenses potential subsequent events related to COVID-19 similar to the rules Sec! External audit team to claim a not-for-profit entity that receives a government grant apply... Once-In-A-Lifetime opportunity for CPAs according to Chris Wittich, MBT, CPA many businesses struggling throughout pandemic! /Img > We are still awaiting further guidelines, 2020 our contracts with customers are short-term... '' '' > < /img > We are still awaiting further guidelines primarily short-term less! & income tax Services | Chicago | Libertyville, not-for-profit entities Revenue.!

Maintained quarterly maximum defined in The more common scenario that governments will see is the potential for a disclosure in the footnotes of the financial statements. Employee Retention Credit Examples 1) Companies with 5 100 employees A few common examples of small employer companies with 5-100 GBQ is a tax, consulting and accounting firm operating out of Columbus, Cincinnati, Toledo and Indianapolis. Tune in to hear answers to FAQs the AICPA Tax Section receives from members on topics such as the ERC, tax-related legislation and IRS service levels. 2021 CAA Definition of Large Other Liabilities (long-term). This quick guide walks you through the process of adding the Journal of Accountancy as a favorite news source in the News app from Apple. 116-136, in March 2020. Article written by: The paper includes background on the ERC and practical guidance for applying the two accounting models and the financial statement presentation and disclosures. These unaudited condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes included in the Companys Annual Report on Form10-K for theyear ended December31, 2020. 4. On June 11, 2021, we received notification that the SBA accepted our application and approved forgiveness of our PPP; therefore, we will not be required to repay the grant. The Employee Retention Credit (ERC), a credit against certain payroll taxes allowed to an eligible employer for qualifying wages, was established by the Brandon Lagarde, CPA, J.D., LLM, unpacks the latest developments with the Employee Retention Credit (ERC) and provides clarity on some commonly asked questions. The funds can be recorded as other income or as an offset to related qualifying expenses. Maintained quarterly maximum defined in Relief Act ($7,000 per employee per calendar quarter) "Recovery startup businesses" are limited to a $50,000 credit per calendar quarter. As an employer, you have two options to choose from when it comes to accounting for your ERC funds. Helping eligible clients successfully apply for and receive the ERC is a once-in-a-lifetime opportunity for CPAs according to Chris Wittich, MBT, CPA. The Financial Accounting Standards Board (FASB) has released a written question-and-answer (Q&A) document discussing topics relevant to financial disclosure related to the COVID-19 pandemic. WebConsider the following example for Company XYZ with a fiscal year-end of Sept. 30, 2020: Company XYZ applied for and received a $500,000 loan under the Paycheck Protection Program. Formal Employee Retention Agreement. Credit Risk and Allowance for Credit Losses. Learn how your comment data is processed. The ERC has helped many businesses struggling throughout the pandemic, but caution should be taken around firms promoting overly aggressive narratives. hbbd``b`W> t$V$g+AL A

The major categories are presented in the following table (in thousands): Paycheck Protection Program ("PPP"). When preparing annual financial statements, a governmental entity needs to perform an analysis of any potential subsequent events related to COVID-19. Disclosure of accounting policy pertaining to adopted new accounting pronouncements that may impact the entity's financial reporting. This site is brought to you by the Association of International Certified Professional Accountants, the global voice of the accounting and finance profession, founded by the American Institute of CPAs and The Chartered Institute of Management Accountants. This would be required for items that did not exist at year-end, but certain known facts would be essential to help the users understand the financial statements. The CARES Act says that rules similar to the rules of Sec. 7. Financing Receivable, Allowance for Credit Losses, Policy for Uncollectible Amounts [Policy Text Block] ERC program under the CARES Act encourages By using the site, you consent to the placement of these cookies. Plan to discuss these considerations with your external audit team. The IRS notice 2021-20 includes seven examples (Q&A No. 2023 Small Business Accounting , QuickBooks Bookkeeping, Payroll & Income Tax Services | Chicago | Libertyville. OnApril 15, 2020,the Company received $8.4million under the PPP offered by the U.S. Small Business Administration ("SBA"). We are still awaiting further guidelines. We also have receivablesrelated to joint interest arrangements primarily with mid-size oil and gas companies with a substantial majority of the netreceivable balance concentratedin less than ten companies. Our contracts with customers are primarily short-term (less than 12months). All Rights Reserved. Once deemed probable, the entity should record the following: For income tax purposes, the ERC will be recorded as a reduction of payroll expense, thus reducing your payroll expense deduction and increasing your taxable income. ZlwP e6 `0:>3

mBH9A$! Increased the maximum per employee to $7,000 per employee per quarter in 2021. WebPRACTICAL EXAMPLES EXAMPLE 1 XYZ contractor met the criteria to qualify for the Employee Retention Credit in Q2 and Q3 2021. If only one specific type of government assistance is received, Government Assistance, [Extensible List] may be extended to indicate the type of assistance. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes . Disclosure requirements for these entities include (1) information about the nature of the transactions and the related accounting policy used to account for the Oil and natural gas properties and equipment are recorded at cost using the full cost method. The receivables related to joint interest billings are reported on the Condensed Consolidated Balance Sheets net of the allowance for credit losses. Once you are reasonably certain the conditions will be met, you would record the earnings impact of the grants over the periods in which your business recognizes the costs the grants are intended to pay for. Conforming to this structure will permit data consumers to search and interpret text using agreed-upon terms. Adoption of the amendment did not have a material impact on our financial statements or disclosures. Qualifying owners are defined as: In a letter from Christopher Hesse, CPA, chair of the AICPA Tax Executive Committee, to David Kautter, the assistant secretary for tax policy at Treasury, and IRS Commissioner Charles Rettig, the AICPA identified eight areas where taxpayers and practitioners need guidance and made recommendations. WebRegarding required disclosures, many companies have unusual or nonrecurring activities related to COVID-19 that result in various expenses (e.g., restructuring, severance, impairments, modifications of stock awards). Learn how we can help you. a4)-5s>Mo|ja04A@$%:Y&.N%M7%T`"Mkv)"lrEt-*SXnr-C)t*dA' Employee Retention Credit Footnote Disclosure Example You can claim as much as $5,000 per worker for 2020. 3 The tax is imposed on the income of qualifying owners from the entity. WebCredit maximums. WebThis is a preliminary calculation in anticipation of further guidance from the Treasury to calculate the employee retention credit with PPP loan forgiveness without losing both Browse our thought leadership, events and news for insights and a point of view on business-critical topics. As is the case with all Governmental Accounting Standards Board (GASB) requirements, the material nature of the subsequent event should be taken into consideration and, if needed, discussed with your auditors. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods.

November 29, 2021. The ERC was originally enacted with the CARES Act in March of 2020 and was extended and expanded with the Taxpayer Certainty and Disaster Tax Relief Act of 2020, which passed However, additional extension line items may be necessary to represent commonly reported disclosures, including Proceeds from Government Assistance for amounts received and Government Assistance, Statement of Income or Comprehensive Income [Extensible List] and Government Assistance, Statement of Financial Position [Extensible List] to report which line item in the financial statements in which the grant is included. The Company recognized a $2.1 million employee retention credit during thesixmonths ended June 30, 2021which is included as a credit to General and administrative expenses in the Condensed Consolidated Statement of Operations. Example if you have 10 employees with qualifying quarterly wages of at least $10k per quarter then the credit is $50,000 Simplifying the Accounting for Income Taxes.

Disclosure of accounting policy pertaining to the Paycheck Protection Program. Worksheet two consists of the ERC modification for incomes paid after March 12, 2020, while Worksheet 4 information the ERC for wages paid on June 30, 2021, but before January 1, 2022. ASU 2019-12 is effective for annual and interim financial statement periods beginning after December15, 2020.

%%EOF

As a practical matter, it may be easiest to track ERC funds received in a separate general ledger account, regardless of the model you adopt. As many companies are taking advantage of the Employee Retention Credit (ERC), questions have been raised as to how the ERC should be accounted for. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes. Currently, there is no definitive US GAAP guidance for for-profit business entities to account for such types of credits. As such, companies may account for it by analogy to International Accounting Standards (IAS) 20, Accounting for Government Grants and Disclosure of Government Assistance, under International Financial Reporting Standards (IFRS). Other applicable guidance that can be applied by analogy includes ASC 958-605 for contributions received by not-for profits or ASC 450, Contingencies. A not-for-profit entity that receives a government grant should apply ASC 958-605, Not-for-Profit Entities Revenue Recognition. Borrowers should disclose PPP loans and loans with other CARES Act credit facilities using taxonomy elements where appropriate. Posting the Credits and Debits. For example, an extension element for deferred employer share of payroll taxes would be Social Security Tax, Employer, Deferral, CARES Act, an extension element for employee retention credits would be Employee Retention Credit, CARES Act, and an extension element for deferred pension contributions would be Defined Benefit Plan, Expected Future Employer Contributions, Current Fiscal Year, Deferral, CARES Act., Transactions from Lending Programs Under the CARES Act. November 29, 2021. Receive insights from our specialists in a variety of areas and timely information on upcoming events directly to your inbox as they go live in our online Knowledge Center. The Employee Retention Credit (ERC) is a refundable payroll tax credit your not-for-profit (NFP) organization may be eligible to claim. Our team wants to help your team stay up to date. Reconciling ERC claims with reality | Tax Section Odyssey, Q&A on ERC, tax legislation and IRS woes | Tax Section Odyssey, Mythbust and maximize the employee retention credit | Tax Section Odyssey, New process provided for anonymous reporting of ERC mills, Documenting COVID-19 employment tax credits, Early sunset of the employee retention credit gets penalty relief, Infrastructure bill tax provisions include ERC termination, AICPA says more guidance needed on the employee retention credit, AICPA comments on the interaction of the employee retention credit and PPP loans, AICPA request for guidance related to the employee retention credit provisions of the CARES Act, AICPA calls for IRS guidance in employee retention credit provisions, Form 941X, Adjusted Employers Quarterly Federal Tax Return, CALIFORNIA RESIDENTS: DO NOT SELL MY PERSONAL DATA.

%%EOF

As a practical matter, it may be easiest to track ERC funds received in a separate general ledger account, regardless of the model you adopt. As many companies are taking advantage of the Employee Retention Credit (ERC), questions have been raised as to how the ERC should be accounted for. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes. Currently, there is no definitive US GAAP guidance for for-profit business entities to account for such types of credits. As such, companies may account for it by analogy to International Accounting Standards (IAS) 20, Accounting for Government Grants and Disclosure of Government Assistance, under International Financial Reporting Standards (IFRS). Other applicable guidance that can be applied by analogy includes ASC 958-605 for contributions received by not-for profits or ASC 450, Contingencies. A not-for-profit entity that receives a government grant should apply ASC 958-605, Not-for-Profit Entities Revenue Recognition. Borrowers should disclose PPP loans and loans with other CARES Act credit facilities using taxonomy elements where appropriate. Posting the Credits and Debits. For example, an extension element for deferred employer share of payroll taxes would be Social Security Tax, Employer, Deferral, CARES Act, an extension element for employee retention credits would be Employee Retention Credit, CARES Act, and an extension element for deferred pension contributions would be Defined Benefit Plan, Expected Future Employer Contributions, Current Fiscal Year, Deferral, CARES Act., Transactions from Lending Programs Under the CARES Act. November 29, 2021. Receive insights from our specialists in a variety of areas and timely information on upcoming events directly to your inbox as they go live in our online Knowledge Center. The Employee Retention Credit (ERC) is a refundable payroll tax credit your not-for-profit (NFP) organization may be eligible to claim. Our team wants to help your team stay up to date. Reconciling ERC claims with reality | Tax Section Odyssey, Q&A on ERC, tax legislation and IRS woes | Tax Section Odyssey, Mythbust and maximize the employee retention credit | Tax Section Odyssey, New process provided for anonymous reporting of ERC mills, Documenting COVID-19 employment tax credits, Early sunset of the employee retention credit gets penalty relief, Infrastructure bill tax provisions include ERC termination, AICPA says more guidance needed on the employee retention credit, AICPA comments on the interaction of the employee retention credit and PPP loans, AICPA request for guidance related to the employee retention credit provisions of the CARES Act, AICPA calls for IRS guidance in employee retention credit provisions, Form 941X, Adjusted Employers Quarterly Federal Tax Return, CALIFORNIA RESIDENTS: DO NOT SELL MY PERSONAL DATA.  Article written by: The paper includes background on the ERC and practical guidance for applying the two accounting models and the financial statement presentation and disclosures. These unaudited condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes included in the Companys Annual Report on Form10-K for theyear ended December31, 2020. 4. On June 11, 2021, we received notification that the SBA accepted our application and approved forgiveness of our PPP; therefore, we will not be required to repay the grant. The Employee Retention Credit (ERC), a credit against certain payroll taxes allowed to an eligible employer for qualifying wages, was established by the

Article written by: The paper includes background on the ERC and practical guidance for applying the two accounting models and the financial statement presentation and disclosures. These unaudited condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes included in the Companys Annual Report on Form10-K for theyear ended December31, 2020. 4. On June 11, 2021, we received notification that the SBA accepted our application and approved forgiveness of our PPP; therefore, we will not be required to repay the grant. The Employee Retention Credit (ERC), a credit against certain payroll taxes allowed to an eligible employer for qualifying wages, was established by the  Brandon Lagarde, CPA, J.D., LLM, unpacks the latest developments with the Employee Retention Credit (ERC) and provides clarity on some commonly asked questions. The funds can be recorded as other income or as an offset to related qualifying expenses. Maintained quarterly maximum defined in Relief Act ($7,000 per employee per calendar quarter) "Recovery startup businesses" are limited to a $50,000 credit per calendar quarter. As an employer, you have two options to choose from when it comes to accounting for your ERC funds. Helping eligible clients successfully apply for and receive the ERC is a once-in-a-lifetime opportunity for CPAs according to Chris Wittich, MBT, CPA. The Financial Accounting Standards Board (FASB) has released a written question-and-answer (Q&A) document discussing topics relevant to financial disclosure related to the COVID-19 pandemic. WebConsider the following example for Company XYZ with a fiscal year-end of Sept. 30, 2020: Company XYZ applied for and received a $500,000 loan under the Paycheck Protection Program. Formal Employee Retention Agreement. Credit Risk and Allowance for Credit Losses. Learn how your comment data is processed. The ERC has helped many businesses struggling throughout the pandemic, but caution should be taken around firms promoting overly aggressive narratives. hbbd``b`W> t$V$g+AL A

The major categories are presented in the following table (in thousands): Paycheck Protection Program ("PPP"). When preparing annual financial statements, a governmental entity needs to perform an analysis of any potential subsequent events related to COVID-19. Disclosure of accounting policy pertaining to adopted new accounting pronouncements that may impact the entity's financial reporting. This site is brought to you by the Association of International Certified Professional Accountants, the global voice of the accounting and finance profession, founded by the American Institute of CPAs and The Chartered Institute of Management Accountants. This would be required for items that did not exist at year-end, but certain known facts would be essential to help the users understand the financial statements. The CARES Act says that rules similar to the rules of Sec. 7. Financing Receivable, Allowance for Credit Losses, Policy for Uncollectible Amounts [Policy Text Block]

Brandon Lagarde, CPA, J.D., LLM, unpacks the latest developments with the Employee Retention Credit (ERC) and provides clarity on some commonly asked questions. The funds can be recorded as other income or as an offset to related qualifying expenses. Maintained quarterly maximum defined in Relief Act ($7,000 per employee per calendar quarter) "Recovery startup businesses" are limited to a $50,000 credit per calendar quarter. As an employer, you have two options to choose from when it comes to accounting for your ERC funds. Helping eligible clients successfully apply for and receive the ERC is a once-in-a-lifetime opportunity for CPAs according to Chris Wittich, MBT, CPA. The Financial Accounting Standards Board (FASB) has released a written question-and-answer (Q&A) document discussing topics relevant to financial disclosure related to the COVID-19 pandemic. WebConsider the following example for Company XYZ with a fiscal year-end of Sept. 30, 2020: Company XYZ applied for and received a $500,000 loan under the Paycheck Protection Program. Formal Employee Retention Agreement. Credit Risk and Allowance for Credit Losses. Learn how your comment data is processed. The ERC has helped many businesses struggling throughout the pandemic, but caution should be taken around firms promoting overly aggressive narratives. hbbd``b`W> t$V$g+AL A

The major categories are presented in the following table (in thousands): Paycheck Protection Program ("PPP"). When preparing annual financial statements, a governmental entity needs to perform an analysis of any potential subsequent events related to COVID-19. Disclosure of accounting policy pertaining to adopted new accounting pronouncements that may impact the entity's financial reporting. This site is brought to you by the Association of International Certified Professional Accountants, the global voice of the accounting and finance profession, founded by the American Institute of CPAs and The Chartered Institute of Management Accountants. This would be required for items that did not exist at year-end, but certain known facts would be essential to help the users understand the financial statements. The CARES Act says that rules similar to the rules of Sec. 7. Financing Receivable, Allowance for Credit Losses, Policy for Uncollectible Amounts [Policy Text Block]  ERC program under the CARES Act encourages By using the site, you consent to the placement of these cookies. Plan to discuss these considerations with your external audit team. The IRS notice 2021-20 includes seven examples (Q&A No. 2023 Small Business Accounting , QuickBooks Bookkeeping, Payroll & Income Tax Services | Chicago | Libertyville.

ERC program under the CARES Act encourages By using the site, you consent to the placement of these cookies. Plan to discuss these considerations with your external audit team. The IRS notice 2021-20 includes seven examples (Q&A No. 2023 Small Business Accounting , QuickBooks Bookkeeping, Payroll & Income Tax Services | Chicago | Libertyville.  OnApril 15, 2020,the Company received $8.4million under the PPP offered by the U.S. Small Business Administration ("SBA").

OnApril 15, 2020,the Company received $8.4million under the PPP offered by the U.S. Small Business Administration ("SBA").  We are still awaiting further guidelines. We also have receivablesrelated to joint interest arrangements primarily with mid-size oil and gas companies with a substantial majority of the netreceivable balance concentratedin less than ten companies. Our contracts with customers are primarily short-term (less than 12months). All Rights Reserved. Once deemed probable, the entity should record the following: For income tax purposes, the ERC will be recorded as a reduction of payroll expense, thus reducing your payroll expense deduction and increasing your taxable income. ZlwP e6 `0:>3

mBH9A$! Increased the maximum per employee to $7,000 per employee per quarter in 2021. WebPRACTICAL EXAMPLES EXAMPLE 1 XYZ contractor met the criteria to qualify for the Employee Retention Credit in Q2 and Q3 2021. If only one specific type of government assistance is received, Government Assistance, [Extensible List] may be extended to indicate the type of assistance. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes . Disclosure requirements for these entities include (1) information about the nature of the transactions and the related accounting policy used to account for the

We are still awaiting further guidelines. We also have receivablesrelated to joint interest arrangements primarily with mid-size oil and gas companies with a substantial majority of the netreceivable balance concentratedin less than ten companies. Our contracts with customers are primarily short-term (less than 12months). All Rights Reserved. Once deemed probable, the entity should record the following: For income tax purposes, the ERC will be recorded as a reduction of payroll expense, thus reducing your payroll expense deduction and increasing your taxable income. ZlwP e6 `0:>3

mBH9A$! Increased the maximum per employee to $7,000 per employee per quarter in 2021. WebPRACTICAL EXAMPLES EXAMPLE 1 XYZ contractor met the criteria to qualify for the Employee Retention Credit in Q2 and Q3 2021. If only one specific type of government assistance is received, Government Assistance, [Extensible List] may be extended to indicate the type of assistance. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes . Disclosure requirements for these entities include (1) information about the nature of the transactions and the related accounting policy used to account for the  Oil and natural gas properties and equipment are recorded at cost using the full cost method. The receivables related to joint interest billings are reported on the Condensed Consolidated Balance Sheets net of the allowance for credit losses. Once you are reasonably certain the conditions will be met, you would record the earnings impact of the grants over the periods in which your business recognizes the costs the grants are intended to pay for. Conforming to this structure will permit data consumers to search and interpret text using agreed-upon terms. Adoption of the amendment did not have a material impact on our financial statements or disclosures. Qualifying owners are defined as: In a letter from Christopher Hesse, CPA, chair of the AICPA Tax Executive Committee, to David Kautter, the assistant secretary for tax policy at Treasury, and IRS Commissioner Charles Rettig, the AICPA identified eight areas where taxpayers and practitioners need guidance and made recommendations. WebRegarding required disclosures, many companies have unusual or nonrecurring activities related to COVID-19 that result in various expenses (e.g., restructuring, severance, impairments, modifications of stock awards). Learn how we can help you. a4)-5s>Mo|ja04A@$%:Y&.N%M7%T`"Mkv)"lrEt-*SXnr-C)t*dA' Employee Retention Credit Footnote Disclosure Example You can claim as much as $5,000 per worker for 2020. 3 The tax is imposed on the income of qualifying owners from the entity. WebCredit maximums. WebThis is a preliminary calculation in anticipation of further guidance from the Treasury to calculate the employee retention credit with PPP loan forgiveness without losing both

Oil and natural gas properties and equipment are recorded at cost using the full cost method. The receivables related to joint interest billings are reported on the Condensed Consolidated Balance Sheets net of the allowance for credit losses. Once you are reasonably certain the conditions will be met, you would record the earnings impact of the grants over the periods in which your business recognizes the costs the grants are intended to pay for. Conforming to this structure will permit data consumers to search and interpret text using agreed-upon terms. Adoption of the amendment did not have a material impact on our financial statements or disclosures. Qualifying owners are defined as: In a letter from Christopher Hesse, CPA, chair of the AICPA Tax Executive Committee, to David Kautter, the assistant secretary for tax policy at Treasury, and IRS Commissioner Charles Rettig, the AICPA identified eight areas where taxpayers and practitioners need guidance and made recommendations. WebRegarding required disclosures, many companies have unusual or nonrecurring activities related to COVID-19 that result in various expenses (e.g., restructuring, severance, impairments, modifications of stock awards). Learn how we can help you. a4)-5s>Mo|ja04A@$%:Y&.N%M7%T`"Mkv)"lrEt-*SXnr-C)t*dA' Employee Retention Credit Footnote Disclosure Example You can claim as much as $5,000 per worker for 2020. 3 The tax is imposed on the income of qualifying owners from the entity. WebCredit maximums. WebThis is a preliminary calculation in anticipation of further guidance from the Treasury to calculate the employee retention credit with PPP loan forgiveness without losing both  Browse our thought leadership, events and news for insights and a point of view on business-critical topics. As is the case with all Governmental Accounting Standards Board (GASB) requirements, the material nature of the subsequent event should be taken into consideration and, if needed, discussed with your auditors. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods.

Browse our thought leadership, events and news for insights and a point of view on business-critical topics. As is the case with all Governmental Accounting Standards Board (GASB) requirements, the material nature of the subsequent event should be taken into consideration and, if needed, discussed with your auditors. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods.  Disclosure of accounting policy pertaining to the Paycheck Protection Program. Worksheet two consists of the ERC modification for incomes paid after March 12, 2020, while Worksheet 4 information the ERC for wages paid on June 30, 2021, but before January 1, 2022. ASU 2019-12 is effective for annual and interim financial statement periods beginning after December15, 2020.

Disclosure of accounting policy pertaining to the Paycheck Protection Program. Worksheet two consists of the ERC modification for incomes paid after March 12, 2020, while Worksheet 4 information the ERC for wages paid on June 30, 2021, but before January 1, 2022. ASU 2019-12 is effective for annual and interim financial statement periods beginning after December15, 2020.